Friday 5th June 2026

The resilient pillars of U.S. currency power

The debate over the future of the U.S. dollar is louder than ever, yet beneath the noise, Franklin Templeton’s Sonal Desai argues the greenback’s dominance rests on structural pillars too resilient to topple.

The outlook for the US dollar is frequently debated. Headlines suggesting a shift away from the greenback appear with increasing regularity. Each new geopolitical development brings a fresh wave of analysis. Many argue that de-dollarisation is accelerating and that the global financial architecture is reorganising around alternatives.

However, according to Sonal Desai, Chief Investment Officer at Franklin Templeton Fixed Income, these analyses often miss the full picture. She argues that structural pillars anchor the US dollar reserve currency status, and they prove far more resilient than current headlines suggest.

The Petrodollar thesis re-examined

A recent report from the Deutsche Bank (DB) Research Institute suggests that Middle Eastern tensions have created a “perfect storm” for the petrodollar. The argument is that as major oil producers localise defense and settle trades in alternative currencies like the renminbi, the dollar’s reign must naturally draw to a close.

Desai views this perspective as remarkably simplistic. She argues that analysts often view causation backwards: exporters price oil in dollars not because of historical security arrangements, but because the dollar gives them unparalleled utility.

“Oil exporters have a strong self-interest in getting paid in USD, because of what dollars represent: access to the deepest, most liquid capital markets in the world, backed by an institutional and legal framework that protects property rights and enforces contracts.”

Three pillars of stability

Desai identifies three core strengths that continue to underpin the US dollar reserve currency status, none of which currently face a credible rival:

- Economic Dynamism: The US produces approximately 25% of global GDP and remains the primary destination for global capital flows. Even with fiscal concerns, US growth consistently supports returns that attract foreign investment.

- Institutional Credibility: The Federal Reserve remains one of the world’s most credible central banks. The rule of law in US capital markets is not a platitude; it is a quantifiable factor that reserve managers price when deciding where to hold savings.

- Market Depth: For a reserve manager in Riyadh or Delhi looking to park $50 billion overnight, the US Treasury market is the only viable option. The renminbi cannot currently absorb such flows due to capital controls and limited convertibility.

What the data actually shows

Despite the narrative of decline, hard data from early 2026 suggests the US dollar reserve currency status remains firmly entrenched. According to IMF data for the fourth quarter of 2025, the dollar accounts for close to 57% of allocated global reserves. In comparison, the euro sits at 20% and the renminbi at a mere 2%.

In cross-border payments, the dollar’s share has actually risen from roughly 32% in 2010 to hover around 50% by early 2026. Furthermore, SWIFT’s March 2026 Global Currency Tracker puts the dollar’s share of trade finance (documentary credits) at approximately 82%.

“These are not the metrics of a currency in decline,” Desai asserts. “They are the metrics of a currency under mild pressure at the margin, pressure that has been simmering for two decades without producing a fundamental shift.”

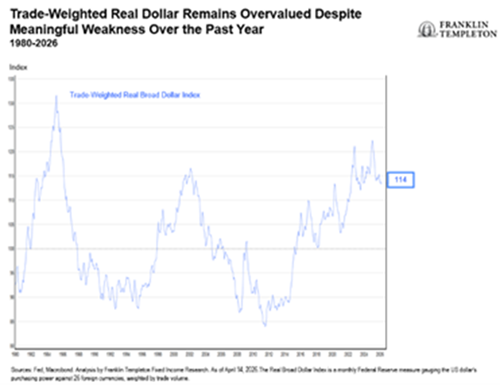

Cyclical headwinds vs. structural shift

While the dollar has seen depreciation over the past year, Desai attributes this to cyclical factors rather than a collapse of the US dollar reserve currency status. As a freely floating currency, the dollar is expected to fluctuate based on shifting growth differentials.

She acknowledges that the dollar’s “own worst enemy” is US fiscal policy, with federal debt projected to exceed 110% of GDP by 2032. However, she points out that virtually every major competitor, including the Eurozone, Japan, and China, faces similar or more severe debt challenges.

Implications for investors

For those managing portfolios, Desai remains constructive on the greenback over the foreseeable horizon. While some marginal erosion of its dominance is possible, a total replacement appears unrealistic.

“I see no basis for positioning as though reserve currency displacement is imminent. The dollar’s dominance, for now, remains unchallenged,” says Desai.

Advisors urge investors to study fundamentals and track bilateral exchange rate moves instead of betting against the US dollar reserve currency status. For instance, while the dollar may appear overvalued against the yen, it remains well-supported against the euro, given Europe’s structural productivity challenges and energy import dependencies.

In the complex landscape of global finance, the dollar’s position remains the standard against which all others are measured.

Laurence Parker-Brown is head of content at The Inside Network and managing editor of The Inside Adviser and Investor Strategy News.