Thursday 9th March 2023

In falling markets, dollar-cost averaging can help reduce exposure

Dollar-cost averaging allows investors to be in the market for the good days as well as the bad. This can help reduce exposure to market declines, as recent research shines light on the difficulty of timing the market.

Many investors use dollar-cost averaging – investing a set amount of money at regular intervals regardless of the direction of markets – to buy shares in a disciplined and non-emotional way. This makes good sense when share markets are falling, but any strategic advantage ends there, strategists say.

Dollar-cost averaging allows investors to be in the market for the good days as well as the bad. And for those who don’t have a large amount to invest or who like the discipline of investing small amounts over time, it provides an effective alternative strategy to lump-sum investing.

An investor practising dollar-cost averaging could, for example, divide a total investment of $120,000 into 12 equal amounts of $10,000 to be invested each month over a year, irrespective of how markets perform. In contrast, lump-sum investment would see the full $120,000 invested at one time – ideally, when prices are low.

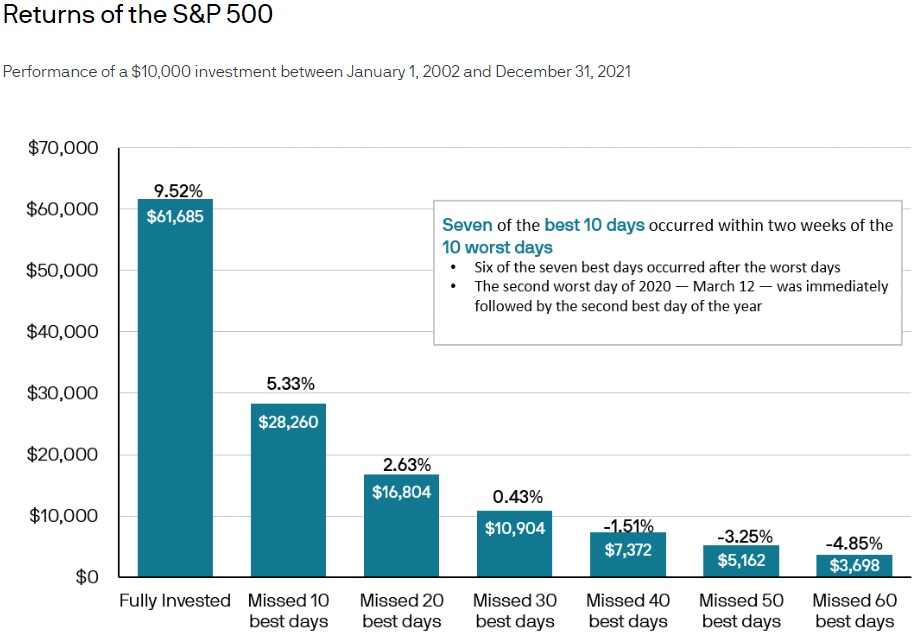

However, market timing is exceedingly difficult, even for professional investors. In a recent paper titled, “Is market timing worth it during periods of intense volatility?”, J.P. Morgan Asset Management global market strategist Jack Manley (pictured) noted that timing the market is almost impossible given that good and bad trading days fall so closely together.

Analysing US return data from 2002 through 2021, the asset manager found that seven of the best 10 trading days occurred within two weeks of the 10 worst days. Often, the gap between the best and worst days was much shorter: for example, March 12 was the second worst day of 2020 in US sharemarkets, and it was immediately followed by the second best day of the year.

And the worst days overwhelmingly occurred before the best days, with six of the seven best trading days of the past 20 years following the worst day.

The close proximity of the best and worst days makes it virtually impossible to buy shares at the bottom before they climb again, analysts say – most people are not that quick or lucky, so it is very unlikely that an investor could consistently miss the worst days while being invested in the market for the best.

Market direction still matters

According to adviser network MLC, dollar-cost averaging is a beneficial strategy when markets are falling. “This is because only a fraction of the total amount to be invested is exposed to declines in the market,” it said. “Also, when the market price falls, your regular investment amount will purchase more investment shares or units, and it may provide a sound savings regime and ideal investment strategy for people with a regular income but without large sums to invest.”

However, when market prices are trending upwards, a lump-sum purchase of assets will produce better results than if those shares were bought using dollar-cost averaging, as the full price gain is captured by the full up-front investment.

Consumer finance website Moneychimp.com provides a calculator that allows users to experiment over different time periods, using historical US market data to compare dollar-cost averaging with lump-sum investing for the specified start date.

Under most circumstances, the lump-sum investment beats the instalment method. “Each strategy wins at least some of the time, but after a few runs you’ll see that [dollar-cost averaging] is the statistical ‘dog’, losing about two times out of three,” the site explained.

Dollar-cost averaging will only win if the start date falls right before a dramatic crash or at the start of a 12-month slump. Without the ability to predict downturns ahead of time, dollar-cost averaging does not provide a distinct advantage.

However, it does have a psychological appeal, according to Moneychimp.com. “If the market dips, people will be happy because [dollar-cost averaging] will be saving them money; and if the market goes up, people will be happy regardless.”

It is almost impossible for any investor to time the market over either the short or the long term. Dollar-cost averaging provides a means to invest without attempting to time the market, while minimising the risk of missing out on the good days.

Nicki is an experienced journalist writing across three publications.