Monday 22nd February 2021

GameStop saga invites scrutiny of brokerage practices

Groups of amateur investors that gather on social media forums such as Reddit have organized to buy stocks and options in companies with high short interest like GameStop, AMC Entertainment and Blackberry, among others. The buying activity drove the stocks up sharply over the last several weeks and resulted in a massive short squeeze with hedge funds forced to cover their shorts in order to limit losses, driving stock prices even higher.

The activity also ratcheted up volatility, causing the pipes that connect equity trading systems across the market to back up, notes ClearBridge Investments, a global equity manager.

In a recent note, the manager says:

In response to the increased volatility in GameStop and other so called “Reddit stocks,” the National Securities Clearing Corporation, which acts as the central clearing counterparty for U.S. equity trading, increased the margins brokerages are required to post. In turn, brokerages placed trading restrictions and raised margin requirements for these stocks on their clients, the retail investors.

Privately held discount broker Robinhood, which has been the subject of numerous fines from regulators in the last year for improper risk and trading data disclosures, drew most of the ire for the trading restrictions from retail investors as well as some members of Congress, including overtures of collusion between the brokerage houses and hedge funds.

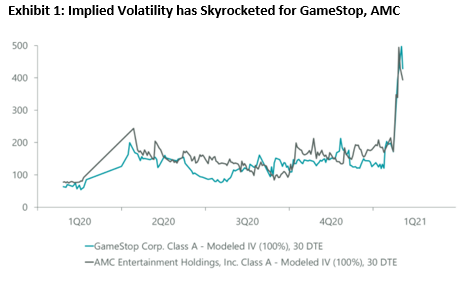

This is not the case as these trading restrictions and elevated margin requirements go hand-in-hand with times of increased volatility and should be viewed as the normal course of business. A similar instance occurred as recently as last March, but current events are garnering more attention given the extreme nature of the volatility occurring in a narrow range of stocks with the backdrop of a Main Street vs. Wall Street showdown (Exhibit 1).

r

Data as of Feb. 2, 2021. Volatility is measured for a composite of near-dated, at the money options with expirations in 30 days over the past year for GME and AMC. Source: FactSet.

Several other online trading platforms, including Interactive Brokers, E*Trade and Charles Schwab, also implemented restrictions to not only protect themselves but limit the potential losses of investors buying these stocks on margin or taking naked short positions, a now illegal practice of selling a stock short when the actual shares have not been borrowed to do so.

Order Flow Could Draw More Attention

The frenzy over the moves in the stock price of GameStop and others also highlighted the role that hedge funds and sophisticated trading firms play in the stock market and the importance of order flow to many of these companies. As greater numbers of investors and others outside of the trading business learn more about what is going on behind the scenes, it will likely lead to greater regulatory and legislative scrutiny of trading activity and market structure.

Discount brokers generate revenue in several ways, with the larger, more established players such as Charles Schwab and E*Trade (now part of Morgan Stanley) having larger balance sheets and more diversified sources of revenue than smaller brokers. These sources include commissions, spread income from investing client cash held in brokerage accounts as well as asset management or distribution fees.

Newer entrants like Robinhood do not charge commissions, have minimal spread income due to small account balances and earn no asset management fees. Instead, they rely on payment for order flow as the primary driver of revenue, whereas it is only a small portion of the more diversified revenue streams seen at larger brokers. Robinhood and its peers sell retail order flow to high frequency trading (HFT) firms. HFT firms pay for the order flow in order to employ algorithmic software to match and trade against the orders at spreads tighter than the exchanges. From a practical standpoint, one could say that the real clients of Robinhood are not day traders and novice individual investors but the HFTs.

Payment for order flow has been around for years but the trading markets have changed a great deal over time. One key difference today is the volume of trading that has moved off stock exchanges like the NYSE and NASDAQ into alternative electronic trading venues.

This has raised concerns about transparency and the ability to obtain best execution on trades. HFTs are significant users of these alternative venues but play a useful role in market structure by providing additional liquidity. If regulators were to prohibit payment for order flow, then a portion of the liquidity that HFTs provide would be removed from the market.

The Securities & Exchange Commission (SEC) issued a statement that they are closely monitoring and evaluating the situation, but changes to market structure regulation tends to occur over a period of years as there is a very thorough process (SEC proposals, comment periods, rule writing, test programs, etc.) to ensure there are no unintended consequences from such changes. We believe there are three potential regulatory items to consider: payment for order flow, increased capital requirements and a financial transaction tax.

We view the latter two items as highly unlikely, but believe that developments on payment for order flow bear watching. Whether or not it played a role in the events that transpired over the last two weeks, it is now in the spotlight and the SEC may take a fresh look at the controversial practice. More stringent stock lending and borrowing rules to limit naked shorting is also a possibility.

Key Takeaways

- The short squeeze battle between individual traders and hedge funds over GameStop and related stocks touted on social media poses a risk to brokers and exchanges as regulators and legislators are expected to take a closer look at broader trading practices and market structure issues.

- Brokers increasing margin requirements and imposing trading restrictions is the normal course of business in times of heightened volatility.

We do not anticipate material bottom-line impacts to brokers and exchanges stemming from this event, but the discussion around payment for order flow bears watching

Miguel del Gallego, CFA

Senior Analyst – Financials

20 Years experience

19 Years at ClearBridge

– See more at: https://www.clearbridge.com/news/blogs/2021/gamestop-invites-scrutiny-brokerage-practices.html#sthash.zPGreLLU.dpuf