Sunday 16th May 2021

Banks boom to send ASX higher on Friday

ASX retakes 7,000, iron ore falls, CBA hits new record, dispersion grows

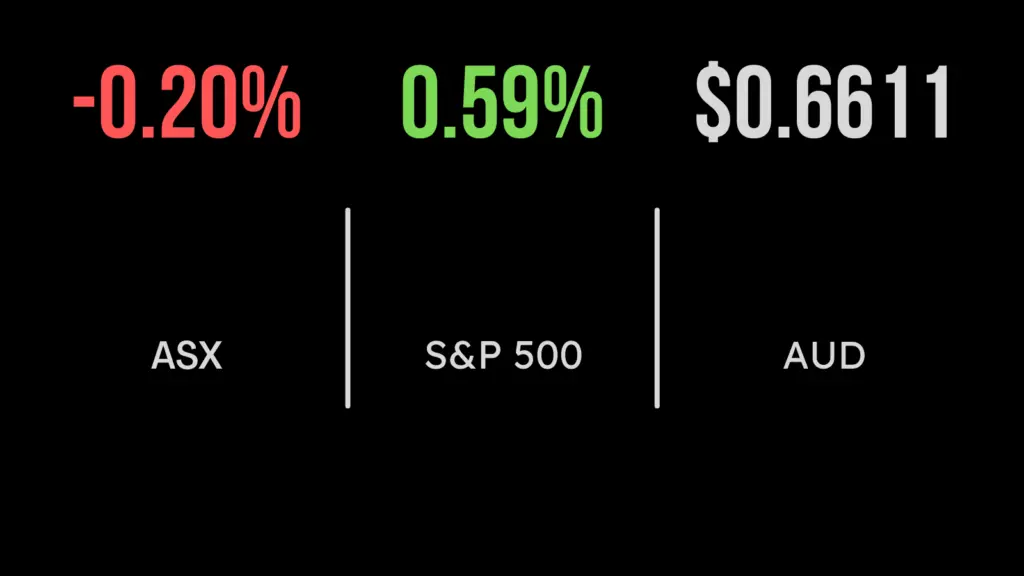

The ASX200 (ASX:XJO) finished the week on a positive note, moving 0.5% higher and retaking the 7,000-point level.

Every sector was higher barring materials, with Fortescue (ASX:FMG) and BHP Group (ASX:BHP) falling 2.8% and 1.5% respectively after the iron ore price dropped 9.5% during the day. On the positive side, the fall in commodity prices has supported a weaker AUD.

Commonwealth Bank of Australia (ASX:CBA) reached a record high (yes, a record!) adding 0.6%, which is quite an achievement given the country is still not past the pandemic.

Over the week dispersion has continued to grow, with more businesses unable to deliver on inflated expectations.

Mining services provider Perenti Global (ASX:PRN) lead the detractors down 28.6%, with A2 Milk (ASX:A2M) and Xero (ASX:XRO) down 21.2% and 15.9% respectively.

The selloff in the tech sector has likely been the news of the week, with the ASX IT index down 6.9% and 20.5% over the last month.

Zip Co (ASX:Z1P) has fallen by half in just three months and AfterPay (ASX:APT) is down 45% since February.

Corporate activity has remained active this week seeing Crown (ASX:CWN) receive two bids, up 6.7% for the week, and Woolworths (ASX:WOW) move forward with their demerger.

Consumer staples and healthcare were the only positive sectors over the week as investors sought safety in ‘defensive’ names.

US market turns the corner, retail sales disappoint, Disney+ subscribers weaker than expected

US markets staged a strong recovery after the worst sell-off in three months, with the Nasdaq leading the way on Friday jumping 2.3%.

The S&P500 and Dow Jones added 1.5% and 1.1% respectively, powered ahead by a recovery in the technology and energy sectors.

The strong sentiment came despite weaker than expected retail sales and consumer confidence, which forced markets to look beyond inflation figures.

Excluding the volatile auto and fuel sales categories, where prices increased over 80%, retail sales actually fell in April by 0.8% as stimulus cheques ran out. Consumer confidence was also well below expected, printing at 82 rather than 90 points.

Over the week all three indices finished lower, the Nasdaq down 2.3%, S&P500 1.4%, and the Dow Jones more resilient falling 1.1% as many constituents fall into the ‘value’ camp.

Walt Disney (NYSE:DIS) was among the big names to report this week, falling around 3% despite reporting a normalised profit of US$912 million for the second quarter.

This was a 32% increase in revenue that fell 13% to US$15.6 billion with the company benefitting from lower production costs and an improvement in advertising.

Disney+ was the detractor, with new subscribers hitting 8.7 million well below the 14.4 million forecasted by analysts.

Short-term focus never greater, searching for quality, betting against the Fed

From the position of writing a daily column my first takeaway may seem counterintuitive, however, having been involved in markets for close to two decades, it is evident that daily news flow is driving markets more than ever.

Whether it is the ease of access to information from sources like Twitter, or the Fear of Missing Out factor that is driving everything from IPOs to crypto, investors must be wary of getting caught up in the short-term noise.

Thankfully, short-termism opens up greater opportunities for patient and informed investors. Speaking with a number of professional investors this week, ‘quality’ has been a clear focus in their stock selection process.

Expanding on the first point, they noted that short-term price momentum and speculation have been a clear driver of the volatility and huge ‘rotations’ we are seeing from defensives to cyclical to growth stocks.

The quality of companies coming to market has been falling and, in some cases, particularly for those digital COVID winners, ranging from Kogan to Redbubble, Adore Beauty, and Nuix, valuations are being driven by extrapolation of extraordinary short-term results.

Finally, it appears that investors are now betting against the Federal Reserve, with traders positioning for a faster than expected increase in interest rates despite multiple confirmations of the opposite.

From a personal perspective, it seems that the fantastic headline economic figures are not reflecting the pain that remains throughout the private sector, particularly for small businesses, and this is clearly the reason that governments and central banks will remain supportive.