Thursday 22nd July 2021

Asian Equities on the right side of disruption

Covid-19 continues to wreak havoc in some parts of Asia, resulting in humanitarian losses that will potentially have a deep and lasting impact on societal values and governance structures. The pandemic has highlighted wide gaps in public health and social security infrastructure that became matters of life and death in some countries.

We believe the pandemic will recede sooner rather than later, but that its impacts will reverberate for years to come. Thus, in the post-Covid world, we may see a significant pivot in resource and capital allocation.

We expect front-loading of many initiatives across Asia in areas such as smart infrastructure (including healthcare infrastructure), increased investments in digitization and automation, and a greater focus on environmental imperatives – all of which embody regional secular trends that could have a meaningful impact on Asia’s equity markets.

Asian equity markets amid the pandemic

Asian equity markets have remained resilient during the pandemic (apart from the deep sell-off in the first quarter of last year, which has since been recouped). Lessons from past crises, including the Spanish flu pandemic of 1918 and the two World Wars, have shown that economies generally build back stronger, and we see few reasons why the outcome would be different today.

We are witnessing two notable drivers behind the resiliency of the region’s business environment: pent-up demand for goods and a digitization-led impulse. The former has resulted in extremely low levels of inventories, which in turn boosted manufacturing activity and fuelled demand for “smart capex,” such as on automation and machinery (see “Asia Equity Trends: The Rise of ‘Steel Collar’ Workers“). The latter has led to a notable increase in digital penetration as firms adjusted to changing customer behaviour, increased work-from-home, and demand for productivity-enhancing and labor-saving technologies.

Both digital leaders and laggards are stepping-up investments: The former want to extend their lead, while the latter want to catch up. Real investment in information processing equipment has been generally robust throughout the pandemic. Moreover, new IT investments in digital areas are forecast to increase (Gartner sees global IT spending growth rising an average 300 basis points (bps) in 2021-2023 from pre-Covid levels), which we see as a tailwind for some of the region’s IT companies.

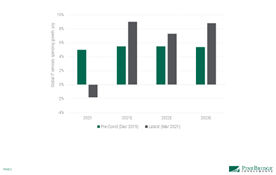

Global IT services spending is expected to accelerate

Source: Gartner as of April 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material. Any opinions, forecasts, and forward-looking statements presented above are valid only as of the date indicated and are subject to change.

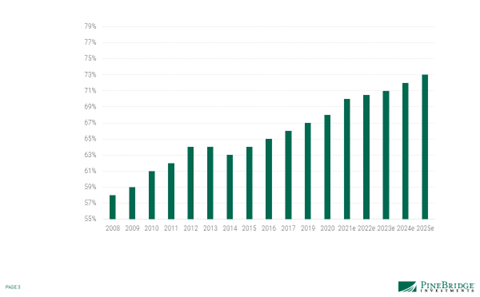

IT outsourcing penetration Is expected to steadily increase

Source: Gartner as of April 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material. Any opinions, forecasts, and forward-looking statements presented above are valid only as of the date indicated and are subject to change.

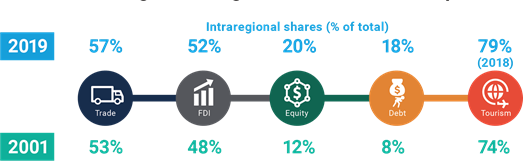

Another source of Asia’s stability is the extent of regional integration. The large share of intra-regional trade (57.5% in 2019) out of the region’s total trade suggests that stronger parts of the region, mostly North Asian economies that have relatively controlled the virus, can serve as a buffer against a slowdown in the rest of the region and could also help drive the overall regional recovery.

Regional integration acts as a buffer against economic slowdowns

Source: Asian Development Bank as of February 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

Near term: Inflation, policy tightening, rotation, and the tech sell-off — threats or opportunities?

We’ve seen a familiar script during most economic or market disruptions: fiscal stimulus, monetary accommodation, release of pent-up demand, and then a recovery taking hold. As growth forecasts for 2021 ratchet up, concerns about long-dormant inflation abound. And it is understandable, too, given that everything from food to commodities (copper included) is soaring and there are shortages of inputs ranging from chips to bicycle components to containers. There’s also a fear that too much stimulus will distort the supply and demand dynamics when some economies are looking to come back on track.

With these latent anxieties, investors turn even more skeptical about central banks’ promises to remain accommodative, starting a selloff in the financial markets. On the ground, we are still witnessing slack in services purchasing managers’ indices (PMIs), stress in small and micro enterprises, and unemployment levels above long-term averages – all signifying that growth has yet to firmly take hold. Therefore, we believe the fear of inflation and ensuing policy tightening in Asia is premature.

Unemployment remains above long-term averages in most Asian economies

Source: Macrobond, PineBridge calculations as of 1 April 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

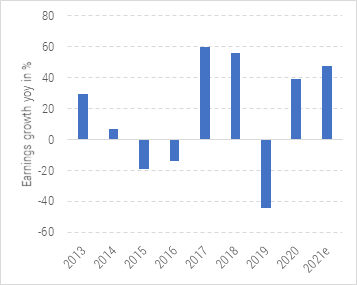

Aside from Covid-19, regulatory changes, geopolitics, and sector-level disruptions continue to transform Asian companies. Take Asian tech. US sanctions and now greater scrutiny over anti-trust practices at home have disrupted China’s tech sector. This has led to a sell-off in some names despite strong first-quarter results and decent forward guidance, on the back of prevailing demand indicators and shortages of semiconductors and other key components (for instance, a leading Japanese original equipment manufacturer recently announced it was halting part of its operations due to component shortages).

Earnings in Asia’s high-tech sector are forecast to increase despite the recent sell-off

Source: Bloomberg as of 17 May 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material. Any opinions, forecasts, and forward-looking statements presented above are valid only as of the date indicated and are subject to change.

Is the sell-off justified? Technology companies had been seen as the best shot to capture Asia’s growth cost-effectively. Their operating leverage made them attractive. Asset-light business models and, often, the lack of physical goods reduce the capital required to a bare minimum. Therefore, tech companies could justify extra-high multiples despite minimal capital and no incremental cost to serve a global addressable market.

Add to this the many unfolding tech-led disruptions that create opportunities in the sector: artificial intelligence, Internet of things, blockchain, edge computing, cloudtech, 5G, cyber-security, data centres, automotive tech demand, and fintech, to name just a few. Thus, we believe investors should concern themselves not with the sell-off itself, but with the right selection of companies that can harness these long-term trends.

Similarly, as the recovery takes hold and companies from other sectors are ready to participate, it is normal for investors to rotate allocations to laggards that they believe are next on the recovery track.

Long term: Environmental imperatives go mainstream

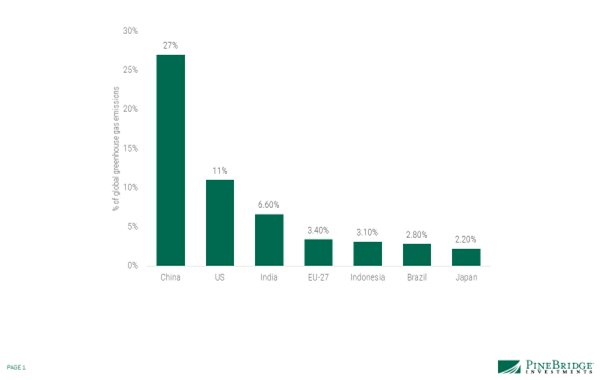

After years of all talk and fizzled expectations, environmental imperatives are on the top of the execution agenda for governments and investors alike. We believe this will be among the strongest forces that could drive growth and investment opportunities in Asia. For instance, China, which accounted for 27% of the world’s emissions in 2019 (followed by the US at 11%)[1] has already pledged to reach net-zero carbon emissions by 2060 – an ambitious goal that will likely bring about a sea-change in the way companies operate in China, the reorganization of the steel industry being a case in point. Similarly, Korea and Japan are also leading in this initiative.

China was the top contributor to global greenhouse gas emissions in 2019

Source: Rhodium Group as of 6 May 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

The lesser-developed parts of the region have also added the environment to their playbook. The high demand for energy in Southeast Asia to sustain its rising economies is beginning to reshape renewable energy regulations. Vietnam is drafting a new power development plan, while the Philippines is implementing renewable portfolio standards and a green energy auction, which will support renewables growth. Indonesia, which had a long history of being a challenging environment for renewables, has an upcoming renewable energy law that could lead to bold changes.

As some of the world’s biggest companies and deepest-pocketed investors line up trillions of dollars to finance a shift away from fossil fuels, opportunities to participate in newer areas such as renewable food chains, storage, grids, fuel cells, eco-friendly mobility, and so forth abound. Once again, we believe being on the side of disruption with the right selection of companies will be the key to future success.

Disruption is an opportunity by another name

We believe the longer the present state of lowered and reconfigured economic activity continues, the stronger the trends toward automation, digitization, environment, and healthcare imperatives will grow, creating numerous investment opportunities over time. While today the pandemic hamstrings some economies and companies, Asia is likely to remain a fast-growing region and will be well anchored into the future. The only requirement in this environment is a robust, time-tested investment philosophy that seeks to uncover quality rather than just ride the trends.

Siddartha Singh is Managing Director of the Asian Equities team at Pinebridge Investments in Hong Kong

[1] Rhodium Group as of 6 May 2021.